Frequently Asked Questions

The System of Environmental-Economic Accounting (SEEA) is an international statistical standard that uses a systems approach to bring together economic and environmental information to measure the contribution of the environment to the economy and the impact of the economy on the environment. The SEEA uses a structure and classifications consistent with the System of National Accounts (SNA) to facilitate the development of indicators and analysis on the economy-environment nexus. This collection of Frequently Asked Questions provides an introduction to the main elements of the SEEA and the concepts of natural capital accounting and ecosystem services.

- What is natural capital?

- What is natural capital accounting?

- What are environmental-economic accounts?

- What is the System of Environmental-Economic Accounts (SEEA)?

- What kind of information does the SEEA provide?

- What are some applications of the SEEA?

- What is ecosystem accounting?

- What are ecosystem services?

- What are ecosystem assets?

- How does the SEEA relate to other official statistics?

- How are SEEA environmental-accounting standards determined?

- How many countries have compiled SEEA accounts?

- Where can I access SEEA datasets?

- How are environmental-economic accounts different than environmental statistics?

- Are monetary values a necessary part of natural capital or environmental economic accounts?

- Does monetary valuation amount to putting a price on nature?

- How does natural capital accounting relate to private sector efforts like the Natural Capital Protocol?

What is natural capital? Return to top

The term 'natural capital' is attributed to economist E.F Schumacher, who presented the concept in his 1973 book Small is Beautiful. There are many definitions of the term. A typical example is the one developed by the Natural Capital Coalition after a a long consultative process:

“Natural capital is another term for the stock of renewable and non-renewable resources (e.g. plants, animals, air, water, soils, minerals) that combine to yield a flow of benefits to people."

Similar definitions can be found in the OECD Glossary of Statistical Terms and the United Nations Glossary of Environmental Statistics.

The concept of natural capital extends beyond nature as a source of raw materials for production (e.g. timber) to include the role of the environment and ecosystems in supporting human well-being through the supply of such important goods and services as clean water, fertile soils and valuable genetic resources.

Since the early 1970s, interest in in the practical applications of a natural capital perspective has grown considerably within government, business, civil society and academic communities.

What is natural capital accounting? Return to top

Natural capital accounting (NCA) is an umbrella term covering efforts to use an accounting framework to provide a systematic way to measure and report on stocks and flows of natural capital. Its underlying premise is that since the environment is important to society and the economy, it should be recognized as an asset that must be maintained and managed, and its contributions (services) be better integrated into commonly used frameworks like the System of National Accounts.

NCA covers accounting for individual environmental assets or resources, both biotic and abiotic (such as water, minerals, energy, timber, fish), as well as accounting for ecosystem assets (e.g. forests; wetlands), biodiversity and ecosystem services.

The SEEA is the accepted international statistical standard for environmental-economic accounting, providing a framework for organizing and presenting statistics on the environment and its relationship with the economy. It brings together economic and environmental information in an internationally agreed set of standard concepts, definitions, classifications, accounting rules and tables to produce internationally comparable statistics.

What are environmental-economic accounts? Return to top

Environmental-economic accounts are integrated statistics that illuminate the relationship between the environment and the economy, both the impacts of the economy on the environment and the contribution of the environment to the economy. Environmental-economic accounts can provide information about the extraction of natural resources, their use within the economy, natural resource stock levels, the changes in those stocks during a specific period and economic activity related to the environment. Environmental-economic accounts present this information in physical and monetary terms, as appropriate.

What is the System of Environmental-Economic Accounting (SEEA)? Return to top

The SEEA is the accepted international standard for environmental-economic accounting, providing a framework for organizing and presenting statistics on the environment and its relationship with the economy. It brings together economic and environmental information in an internationally agreed set of standard concepts, definitions, classifications, accounting rules and tables to produce internationally comparable statistics.

The SEEA is developed and released under the auspices of the United Nations, the European Commission, the Food and Agriculture Organization of the United Nations, the Organisation for Economic Co-operation and Development, International Monetary Fund and the World Bank Group.

It consists of two parts:

- The SEEA Central Framework (SEEA CF) was adopted by the UN Statistical Commission as the first international standard for environmental-economic accounting in 2012. The Central Framework looks at “environmental assets”, such as water resources, energy resources, forests, fisheries, etc., their use in the economy and returns back to the environment in the form of waste, air and water emissions. In addition there are also several methodological documents that have a sectoral approach such as : SEEA-Energy; SEEA-Water and the SEEA Agriculture, Forests and Fisheries (AFF).

- The SEEA Ecosystem Accounting (SEEA EA) complements the Central Framework and was adopted by the UN Statistical Commission in 2021. It takes the perspective of ecosystems and considers how individual environmental assets interact as part of natural processes within a given spatial area. Ecosystem accounts enable the presentation of indicators of the level and value of “ecosystem services” in a given spatial area.

Finally, the SEEA Applications and Extensions illustrates to compilers and users of SEEA Central Framework based accounts how the information can be used in analysis and to derive indicators.

What kind of information does the SEEA provide? Return to top

The SEEA presents information in physical and monetary terms regarding environmental stocks and flows between the environment and the economy as well as economic activity related to the environment. The SEEA provides frameworks for producing accounts in several thematic areas, including:

Agriculture, Forests, and Fisheries Accounts. The System of Environmental-Economic Accounting for Agriculture, Forestry and Fisheries integrates information on the environment and economic activities of agriculture, forestry and fisheries using the structures and principles laid out in the SEEA Central Framework. These activities depend directly on, as well as have an impact upon, the environment and its resources. Integrating information about agriculture, forestry and fisheries facilitates understanding of the trade-offs and dependencies between these activities and their related environmental factors.

Air Emissions Accounts The air emissions accounts in the SEEA provide information on emissions released to the atmosphere by establishments and households as a result of production, consumption and accumulation processes using the structures and principles laid out in the SEEA Central Framework. The air emissions accounts record the generation of air emissions by resident economic units according to type of gaseous or particulate substance.

Energy Accounts SEEA-Energy is a multi-purpose conceptual framework for organizing energy-related statistics. It supports analysis of the role of energy within the economy, the state of energy inputs and various energy-related transactions of environmental interest. Energy information is typically presented in physical terms, but the SEEA-Energy also applies monetary valuations to various stocks and flows, based on the SEEA accounting approach

Environmental Activity Accounts The environmental activity accounts to provide information on transactions concerning activity undertaken to preserve, protect and manage the environment. These accounts follow a purpose-based approach and use the structures and principles laid out in the SEEA Central Framework. Understanding environmental activity is critical to understanding whether economic resources are being used effectively to reduce pressures on the environment and maintain the capacity of the environment to deliver benefits.

Ecosystem Accounts The SEEA Ecosystem Accounting constitutes an integrated statistical framework for organizing biophysical data, measuring ecosystem services, tracking changes in ecosystem assets and linking this information to economic and other human activity.

The SEEA Ecosystem Accounting complements the SEEA Central Framework by taking a different perspective. The Central Framework looks at “individual environmental assets”, such as water resources, energy resources, etc. and how those assets move between the environment and the economy. In contrast, the SEEA Ecosystem Accounting takes the perspective of ecosystems and considers how individual environmental assets interact as part of natural processes within a given spatial area.

Land Accounts These accounts provide information on land use and land cover and can enable an assessment of the changing shares of different land uses and land cover within a country. Understanding these characteristics and changes is critical to understanding the impacts of urbanization, the intensity of crop and animal production, afforestation and deforestation, the use of water resources and other direct and indirect uses of land.

Material Flow Accounts The SEEA Material Flow Accounts can provide an aggregate overview of material inputs and outputs in terms of inputs from the environment, outputs to the environment, and the physical amounts of imports and exports. Understanding economy-wide material flow is critical to understanding resource use by the economy and eco-efficiency.

Water Accounts SEEA-Water is an integrated approach to water monitoring, bringing together a wide range of water related statistics across sectors into one coherent information system. It serves as a conceptual framework and set of accounts which presents hydrological information alongside economic information in a consistent manner.

What are some applications of the SEEA? Return to top

Examples of the kinds of questions that the SEEA can help answer include:

- Who benefits and who is negatively impacted from natural resource use? What are the impacts on the state of the environment and on specific sectors of the economy?

- How does depletion of natural resources affect measures of the real income of a nation? What extracting industries and owners of natural resources are responsible for depletion?

- To what extent is decoupling between resource use and economic growth taking place? Which sectors have the highest water productivity of are most energy intensive?

- How is the wealth of nations, specifically its natural capital, developing over time?

- Are the expenditures on environmental protection effective?

- To what extent is the tax system greening? What economic instruments are in place? And what is the impact of new instruments?

- What is the size of environmental investment in the economy? How many green jobs is the economy generating?

- Are current trends in production and consumption of resources sustainable? Is the amount of waste generated increasing or not; how much of this is being recycled in what economic sectors?

- What is the carbon footprint or water footprint of the nation?

- Which ecosystem services are being generated, who is benefiting from them, and where are they located?

The SEEA Applications and Extensions illustrates to compilers and users of SEEA Central Framework based accounts how the information can be used in analysis and the derivation of indicators.

What is ecosystem accounting? Return to top

Ecosystem accounting is a coherent framework for integrating measures of ecosystems and the flows of services from them with measures of economic and other human activity. Ecosystem accounting complements, and builds on, the accounting for environmental assets as described in the SEEA Central Framework (e.g. water resources, soil resources). In ecosystem accounting as described in the SEEA Ecosystem Accounting, the accounting approach recognizes that these individual resources function in combination within a broader system and within a given spatial area.

It is an approach that can help answer questions such as:

- What is the contribution of ecosystems and their services to the economy, social wellbeing, jobs and livelihoods?

- How is the condition, health and integrity of ecosystems and biodiversity changing over time and where are the main areas of degradation and enhancement?

- How can natural resources and ecosystems be best managed to ensure continued services and benefits such as energy, food supply, water supply, flood control, carbon storage and recreational opportunities?

- What are the trade-offs among different land uses (e.g. for agriculture, mining, housing development, habitat conservation, recreation) to achieve long-term sustainability and equity?

Ecosystem accounting does this by integrating biophysical and economic data using standard accounting principles and accounts to produce detailed measurements of the linkages between ecosystems and economic and other human activity.

Because an ecosystem’s contribution to human well-being is dependent on its location (for example, its proximity to human settlements), ecosystem accounts are inherently spatial.

What kind of information is contained in ecosystem accounts? Return to top

Ecosystem accounting can produce information on the extent of ecosystems, their condition based on selected indicators, and the flow of ecosystem services. Because of the spatial nature of ecosystem accounting, maps are a common method of presenting information. The links between an ecosystem and the economy can be presented in both physical and monetary terms, often via combined presentations that show both kinds of data together, noting that monetary valuation is not a necessary feature of the accounts.

SEEA Ecosystem Accounting is an integrated statistical framework for organizing biophysical data, measuring ecosystem services, tracking changes in ecosystem assets and linking this information to economic and other human activity. It comprises a set of accounts that collectively present a coherent and comprehensive view of ecosystems:

- Ecosystem extent account: This account serves as a common starting point for ecosystem accounting. It organizes information on the extent of different ecosystem types (e.g. forests, wetlands, agricultural areas, marine areas) within a country in terms of area.

- Ecosystem condition account: This account organizes biophysical information on the condition of different ecosystem types. The ecosystem condition account organizes data on selected ecosystem characteristics and the distance to a reference condition to provide insight into the ecological integrity of ecosystems.

- Ecosystem services flow account (physical and monetary terms): This set of ecosystem accounts measures the supply of ecosystem services and the use of those services by economic units, including households, enterprises and government.

- Monetary ecosystem asset account: This account records information on stocks and changes in stocks (additions and reductions) of assets. The ecosystem monetary asset account records this information in monetary terms for ecosystem assets based on the monetary valuation of ecosystem services and applying the net present value approach to obtain opening and closing values in monetary terms for ecosystem assets at the beginning and end of each accounting period.

- Thematic accounts: These accounts organize data on themes of specific policy relevance. Examples of relevant themes include biodiversity, climate change, oceans and urban areas.

What are ecosystem services? Return to top

In the SEEA Ecosystem Accounting, ecosystem services are defined as “the contributions of ecosystems to the benefits that are used in economic and other human activity.”

The SEEA Ecosystem Accounting uses the following three broadly agreed categories of ecosystem services:

- Provisioning services are those ecosystem services representing the contributions to benefits that are extracted or harvested from ecosystems;

- Regulating and maintenance services are those ecosystem services resulting from the ability of ecosystems to regulate biological processes and to influence climate, hydrological and biochemical cycles, and thereby maintain environmental conditions beneficial to individuals and society;

- Cultural services are the experiential and intangible services related to the perceived or actual qualities of ecosystems whose existence and functioning contributes to a range of cultural benefits.

What are ecosystem assets? Return to top

Ecosystem assets are contiguous spaces of a specific ecosystem type characterized by a distinct set of biotic and abiotic components and their interactions. The definition of ecosystem assets is a statistical representation of the general definition of ecosystems from the Convention on Biological Diversity. Examples of ecosystem assets include forests, wetlands, agricultural areas, rivers and coral reefs.

Ecosystem assets are the building blocks for the accounting framework and provide the structure for the organisation of data about ecosystems. Ecosystem assets supply ecosystem services, either from a single ecosystem asset or by multiple ecosystem assets operating collectively. In this framing, ecosystem assets may be characterized as producing units. Ecosystem assets are measured by their extent and condition as well the basket of ecosystem services flows that they generate. Ecosystem assets are nested within the broader concept of environmental assets as defined within the SEEA Central Framework.

Ecosystem assets are classified into ecosystem types, where the IUCN Global Ecosystem Typology is used as reference classification.

How does the SEEA relate to other official statistics? Return to top

The System of National Accounts (SNA) is a measurement framework that has been evolving since the 1950s to embody the pre-eminent approach to the measurement of economic activity, economic wealth and the general structure of the economy. The SEEA Central Framework applies the accounting concepts, structures, rules and principles of the SNA to environmental information. Consequently, the SEEA Central Framework allows for the integration of environmental information (often measured in physical terms) with economic information (often measured in monetary terms) in a single framework. Because it uses the same accounting conventions, the SEEA Central Framework is aligned, in general, with the SNA. For example, SEEA accounts use the “residence principle” in determining boundaries, so that data is based on residence of producer units rather than the territory in which activity occurs, the same approached used for Gross Domestic Product.

How are SEEA environmental-accounting standards determined? Return to top

The UN Committee of Experts on Environmental-Economic Accounting (UNCEEA) was established by the UN Statistical Commission at its 36th session in March 2005. The UNCEEA functions as an intergovernmental body to provide overall vision, coordination, prioritization and direction in the field of environmental-economic accounting and supporting statistics. The UNCEEA meets once a year in New York and is governed by the Bureau of the UNCEEA which convenes regularly between the annual meeting. Its members included representatives from national statistical agencies and international organisations.

Among its roles is to further methodologies and submit recommendations to be adopted by the United Nations Statistical Commission. The Bureau of the Committee of Experts on Environmental-Economic Accounting, consisting of representatives elected among its members and acting under delegated authority from the Committee of Experts, manages and coordinates revisions to the SEEA.

Development of standards involves the contributions of experts from many disciplines and regular consultation with the statistical community and beyond Drafts undergo a global consultative process and during the course of any updates, recommendations and updated text are posted on the SEEA website for worldwide comment, thereby achieving full transparency in the process.

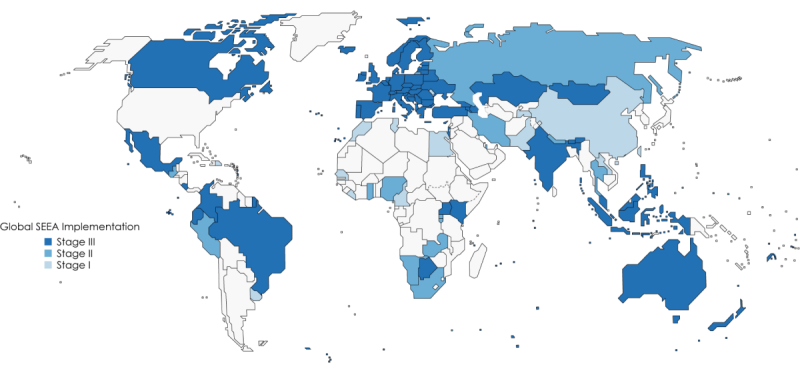

How many countries have compiled environmental-economic accounts? Return to top

As of 2021, 90 countries have compiled SEEA accounts and many more countries are planning to compile the accounts. Find out more about global implementation of the SEEA here.

Note: The designations employed and the presentation of material on this map do not imply the expression of any opinion whatsoever on the part of the Secretariat of the United Nations concerning the legal status of any country, territory, city or area or of its authorities, or concerning the delimitation of its frontiers or boundaries. Final boundary between the Republic of Sudan and the Republic of South Sudan has not yet been determined. Final status of the Abyei area is not yet determined. * Non-Self-Governing Territory. ** Dotted line represents approximately the Line of Control in Jammu and Kashmir agreed upon by India and Pakistan. The final status of Jammu and Kashmir has not yet been agreed upon by the parties. *** A dispute exists between the Governments of Argentina and the United Kingdom of Great Britain and Northern Ireland concerning sovereignty over the Falkland Islands (Malvinas).

Where can I access SEEA datasets? Return to top

Dozens of countries in all regions of the world compile SEEA accounts on a regular basis. The accounts compiled vary based on the priorities of the countries, as well as the available data. Eurostat maintains hosts environmental-accounting data for European countries here.

The UNCEEA has been tasked by the UN Statistical Commission to explore the possibility of having global databases on various SEEA accounts (e.g. air emission account, physical energy supply and use accounts) based on existing data sources. A number of other international organisations, including Eurostat, FAO, OECD and UN Environment, are working in close collaboration with the UNCEEA and UNSD to develop global databases for SEEA accounts.

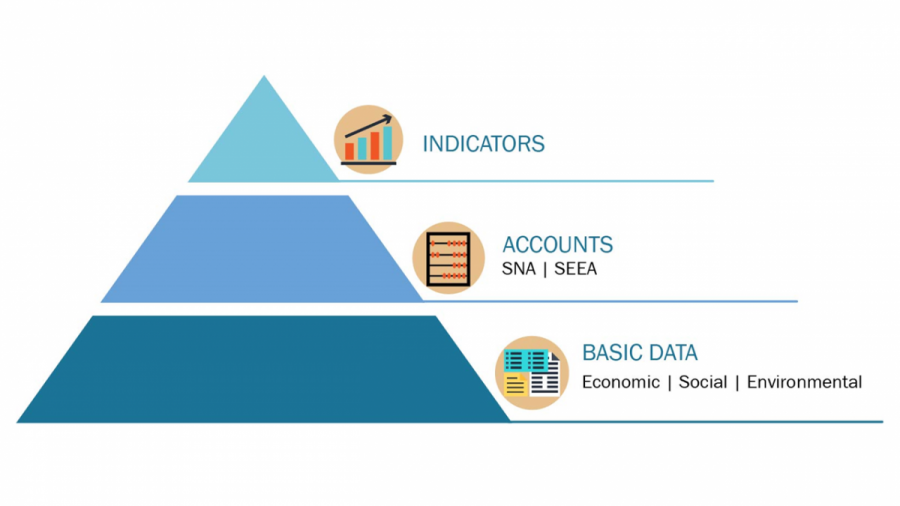

How are environmental-economic accounts different than environmental statistics? Return to top

To place accounting frameworks in context it is relevant to consider the information pyramid. This pyramid has as its base a full range of basic statistics and data from various sources including surveys, censuses, scientific measurement and administrative sources. Generally, these data will be collected for various purposes with the use of different measurement scopes, frequencies, definitions and classifications. Each of these data sources will be relevant to analysis or monitoring of specific themes.

The role of accounting frameworks (at the middle levels of the pyramid) is to integrate these data to provide a single best picture of a broader concept or set of concepts – for example economic growth or ecosystem condition. The compiler of accounts must therefore reconcile and merge data from various sources taking into account differences in scope, frequency, definition and classification as appropriate.

Finally, having integrated the data within a single framework, indicators can be derived that provide insights into the changes in composition, changes in relationships between stocks and flows, and other features taking advantage of the underlying relationships in the accounts between stocks and flows, between capital and labour, between production and consumption, etc. Indicators such as GDP, national saving, national wealth, terms of trade and multi-factor productivity all emerge from the one national accounts framework. Indicators derived from SEEA accounts can be used coherently in conjunction with standard economic indicators.

Are monetary values a necessary part of natural capital or environmental-economic accounts? Return to top

Monetary valuation is possible but by no means required when doing natural capital accounting. There is a significant amount of information in physical terms that can be organized within an accounting framework to support analysis, monitoring and decision making. A key feature of natural capital accounting using the SEEA framework is the organization of information in physical terms to facilitate comparisons with economic data even without monetary valuation.

Information concerning indicators of ecosystem condition may be compiled to provide important information related to quantitative changes in ecosystem condition. The river accounts developed for South Africa that showed a 10% reduction in river health from 1999 to 2011 are an example of how natural capital accounting can generate important information to guide decision making without resorting to monetary valuation.

The issue of monetary valuation raises a range of important ethical and cultural considerations. Attempts to place values on ecosystems in monetary terms may be considered inappropriate and the valuation of ecosystems and the estimated valuations themselves commonly generate the most contention among all measurement issues. Some argue that environmental valuation when market data is limited requires a number of assumptions and hence might be considered outside the domain of official statistics.

Notwithstanding these concerns, there are applications where valuation is seen as supplying useful information for decisionmakers. These include the assessment of specific policies and projects using a benefit-cost framework, the development of environmentally adjusted economic aggregates and raising awareness around the economic contributions of ecosystems, particularly in settings where ecosystems have traditionally been assigned an implicit value of zero. Importantly, while a valuation may be appropriate for one specific decision context, it may be very misleading if applied to others. Therefore, care must be taken in interpreting and communicating valuation estimates to avoid overgeneralizing results.

Does monetary valuation amount to putting a price on nature? Return to top

No. As noted above, monetary valuations are developed within specific decision contexts. For starters, almost no (if any) proponent of valuation believes economic considerations are the only reason to commit to preserving and protecting the natural world. There are ethical and other considerations concerning human beings’ relationship to nature that lie beyond the realm of economic analysis. Furthermore, even within the framework of economics, monetary valuations are generally limited in their scope. Rather than placing a price on nature, valuations are limited to providing an estimate of the economic value of a limited number of services at a time.

Despite its limitations, monetary valuation can in certain contexts help put the preservation of nature on an equal footing with its development, thereby helping decisionmakers more clearly understand attendant trade-offs.

How does natural capital accounting relate to private sector efforts like the Natural Capital Protocol? Return to top

The Natural Capital Protocol (NCP) is a decision making framework that enables organizations to identify, measure and value their direct and indirect impacts and dependencies on natural capital.

The NCP emerged in the private sector and was initially developed with an orientation toward users looking at the firm or project level. It consists of a series of questions or steps to be integrated into existing business operations. It is therefore best understood as a process for incorporating natural concerns into decisionmaking rather than as a set of accounting principles.

As the practice of natural capital accounting has grown in both the private and public sectors worldwide, there has been growing convergence and increasing opportunities for and interest in collaboration between the NCP and SEEA communities. For example, the SEEA offers a framework that can provide useful data for businesses and can serve as a model as the private sector seeks to move toward greater standardisation of methodology. Conversely, the NCP can be an effective tool for a country’s efforts to implement and expand its environmental economic accounting programmes.