Findings from the 2023 Global Assessment of Environmental-Economic Accounting

In late February, UNSD released the results of the 2023 Global Assessment of Environmental-Economic Accounting and Supporting Statistics as a background document for the 55th Session of the Statistical Commission. Administered annually by UNSD under the auspices of the UN Committee of Experts on Environmental Economic Accounting (UNCEEA), the survey provides a comprehensive way to monitor the status and progress of implementation of the System of Environmental-Economic Accounting (SEEA) around the world and also provides data for SDG sub-indicator 15.9.1(b).

This year’s Assessment was administered as a benchmark assessment, which is conducted every three years to obtain information on the specific accounts that countries are compiling, as well as to gather information on institutional arrangements, funding, staffing, technical assistance, future plans, use of the accounts, and policy priorities in countries. The Assessment was sent to all 193 UN Member States as well as 22 territories, with a response rate of 71 per cent (152 respondents).

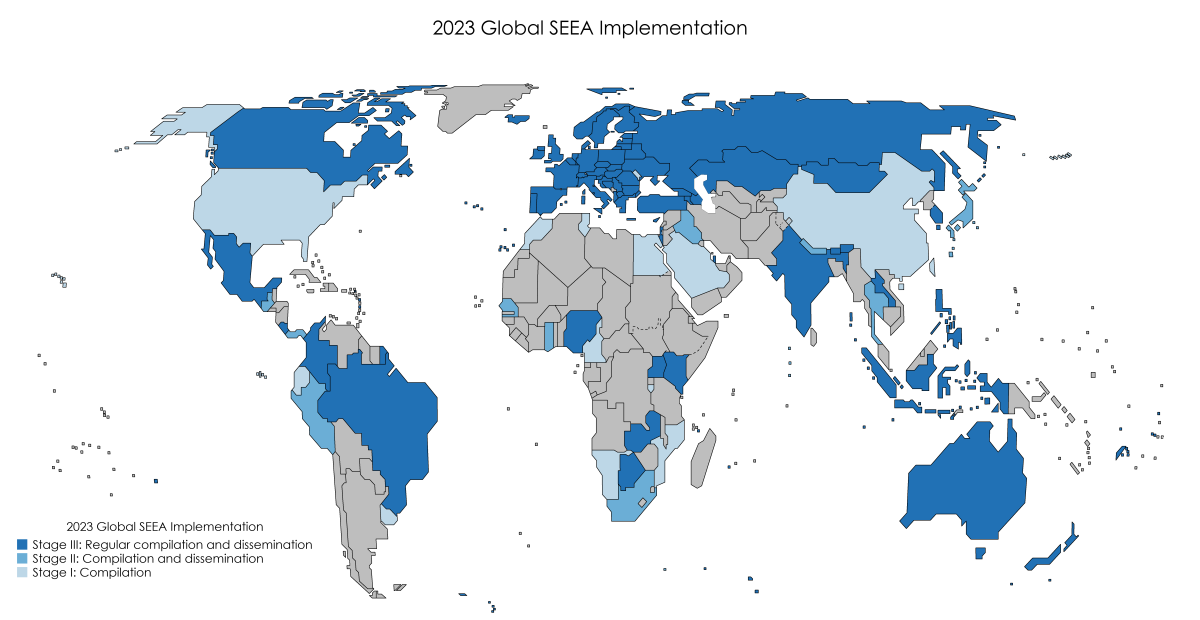

The results of the 2023 benchmark assessment show that 90 countries are implementing[i] the SEEA (see Figure 1).

Figure 1.

The boundaries and names shown, and the designations used on this map do not imply official endorsement or acceptance by the United Nations. Dotted line represents approximately the Line of Control in Jammu and Kashmir agreed upon by India and Pakistan. The final status of Jammu and Kashmir has not yet been agreed upon by the parties. Final boundary between the Republic of Sudan and the Republic of South Sudan has not yet been determined. A dispute exists between the Governments of Argentina and the United Kingdom of Great Britain and Northern Ireland concerning sovereignty over the Falkland Islands (Malvinas).

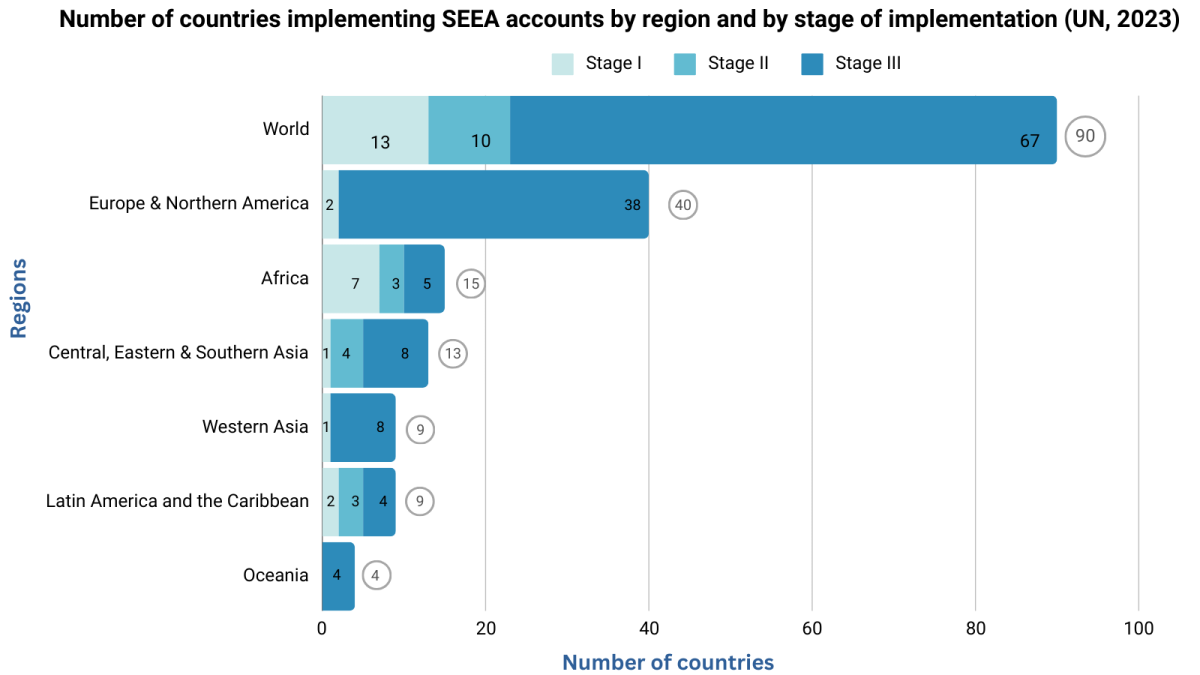

Of these 90 countries, 67 (74 per cent) compile and publish at least one account on a regular basis (stage III); 11 (12 per cent) compile and publish their accounts on an ad-hoc basis (stage II); while 13 countries (14 per cent) compile, but do not yet publish their accounts (stage I). The number of countries implementing SEEA accounts by region and by stage of compilation are shown in Figure 2.

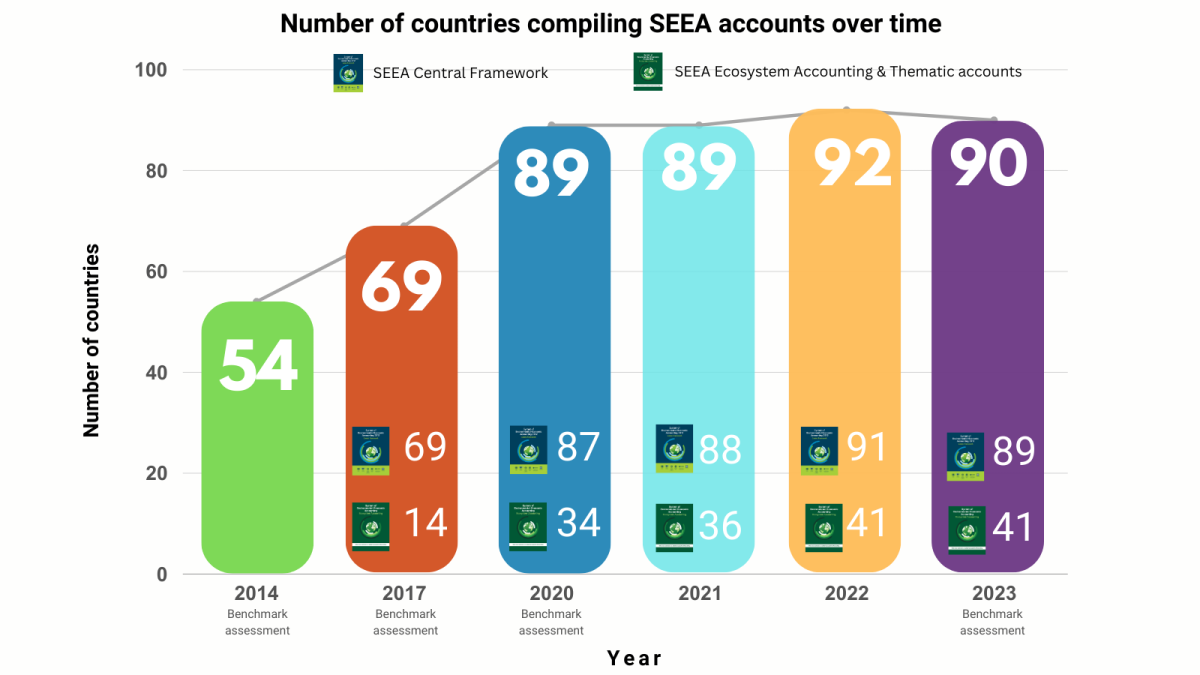

Among the countries implementing SEEA accounts, nearly all (89 out of 90 countries) compile SEEA Central Framework (SEEA CF) accounts. In addition, 41 countries compile SEEA Ecosystem Accounting (SEEA EA) and/or thematic accounts.

Since the last benchmark assessment in 2020, the total number of countries compiling SEEA accounts increased by only one. However, there has been progress in the stage of implementation of countries, with an increase in the number of countries regularly compiling and disseminating SEEA accounts (62 vs 67 countries in the same period). Additionally, between 2020 and 2023, seven more countries began compiling SEEA EA and/or thematic accounts, increasing from 34 to 41. Trends in SEEA implementation are shown in Figure 3.

Future plans and technical assistance

The potential growth of the SEEA is evident by the number of countries that indicated plans to either begin or expand implementation. The vast majority (96 per cent) of implementing countries plan to expand their compilation of the SEEA, and a large majority (48 out of 62, or 77 per cent) of countries that do not currently implement the SEEA intend to initiate implementation in the future.

Technical assistance will be crucial to supporting these implementation efforts. Already, fifty-six per cent of respondents indicated that their country received some kind of technical assistance. For countries compiling SEEA accounts, this figure rises to 78 per cent, with most assistance coming from international organizations.

Institutional landscape for SEEA implementation

In terms of countries’ institutional frameworks for SEEA implementation, 90 per cent of implementing countries indicated that the accounts are compiled by the national statistical office (NSO). However, 47 per cent of countries noted that accounts are compiled in more than one institution within their respective countries, indicating a multistakeholder approach for SEEA implementation.

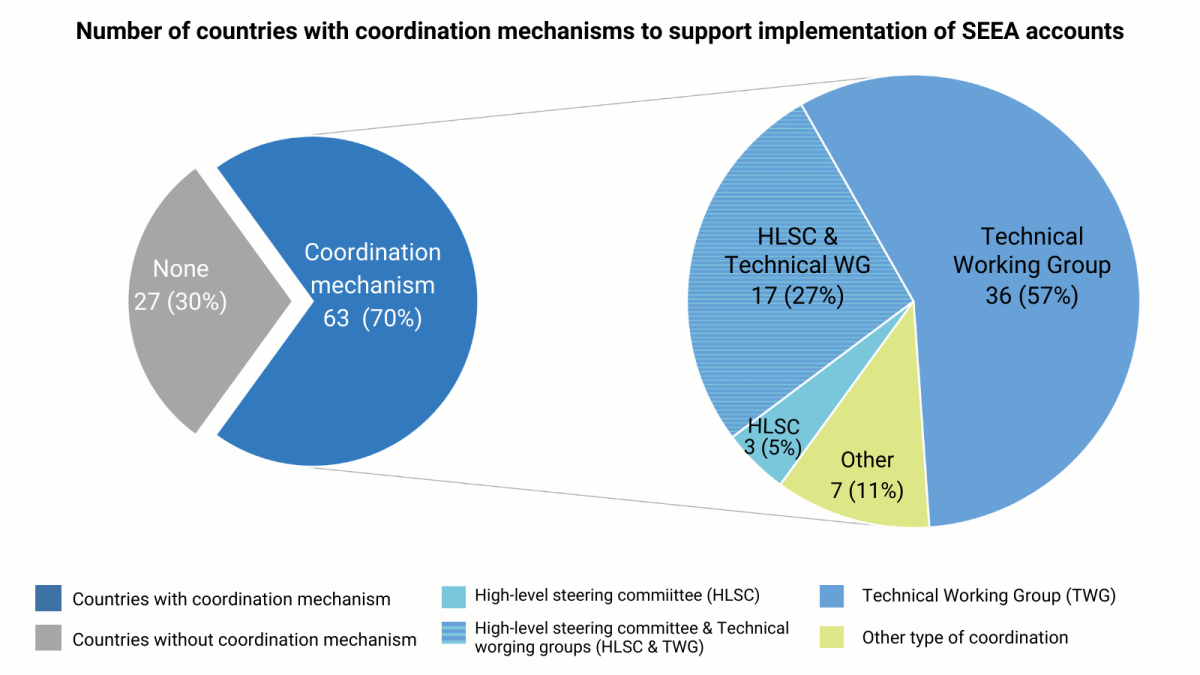

Collaboration among multiple stakeholders (NSOs, line ministries, research institutions, etc.) is facilitated by an array of coordination mechanisms. Out of the 90 countries compiling SEEA accounts, 63 (70 per cent) have established at least one type of coordination group to support the compilation of accounts. Among these, technical working groups are the most used (53 countries), followed by high-level steering committees (20 countries). Most countries with steering committees also have technical working groups, with 17 countries having both. Only three countries are solely reliant on steering committees and 36 solely on technical working groups. The remaining countries use other types of coordination on an ad hoc basis (see Figure 4).

Figure 4.

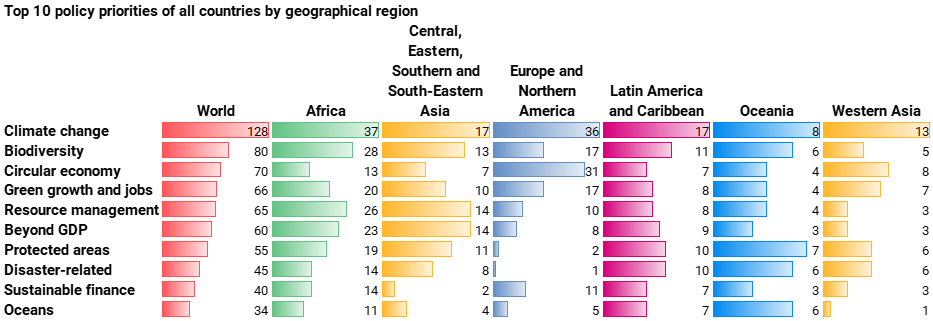

Policy priorities of countries and use of the accounts

The Assessment also collected data regarding various SEEA-related policy priorities across countries. Climate change emerged as the most mentioned priority globally, as well as across all regions. Biodiversity and circular economy ranked as the second and third priorities at a global level, although not always across all regions. Other regional variations were notable, with some countries highlighting resource management, green growth, protected areas, beyond-GDP and/or disaster-related policies, based on their specific contexts (see Figure 5).

Regarding the use of accounts, most countries reported using SEEA accounts for both informing national policies and Sustainable Development Goal (SDG) reporting.

More details can be found in the dedicated page for the Global Assessment here.[i]

[i] Results of the 2023 Global Assessment of Environmental-Economic Accounts have been updated after the publication of the report.

[i] For the purposes of the Assessment, an environmental-economic account is considered compiled if the account has been compiled within the last five years (2019-2023), in physical or in monetary terms, and if this account is consistent with the SEEA (e.g. measurement principles and classifications). Compilation may be on a pilot basis and could be at the subnational level.